The Compliance Moat: Turning 2025 Regulations into a Competitive Advantage

Saheed Aremu

March 26, 2026

Share this article on:

'%3e%3cpath%20d='M0.639648%20-0.000244141H28.2795V27.6396H0.639648V-0.000244141Z'%20fill='black'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M11.0067%205.29028H5.12061L12.0994%2014.5084L5.56705%2022.2413H8.58519L13.5259%2016.3926L17.913%2022.1874H23.7991L16.6175%2012.7014L16.6302%2012.7178L22.8136%205.39793H19.7955L15.2035%2010.8338L11.0067%205.29028ZM8.36963%206.90467H10.2021L20.55%2020.573H18.7176L8.36963%206.90467Z'%20fill='white'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_215_1244'%3e%3crect%20width='27.6398'%20height='27.6398'%20fill='white'%20transform='translate(0.639648)'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

'%3e%3cpath%20d='M0.279785%20-0.000244141H27.9196V27.6396H0.279785'%20fill='black'/%3e%3cpath%20d='M7.94565%209.44696C9.04879%209.44696%209.94306%208.55269%209.94306%207.44956C9.94306%206.34642%209.04879%205.45215%207.94565%205.45215C6.84251%205.45215%205.94824%206.34642%205.94824%207.44956C5.94824%208.55269%206.84251%209.44696%207.94565%209.44696Z'%20fill='white'/%3e%3cpath%20d='M13.4517%2010.4729V21.1617V10.4729ZM7.94531%2010.4729V21.1617V10.4729Z'%20fill='white'/%3e%3cpath%20d='M13.4517%2010.4729V21.1617M7.94531%2010.4729V21.1617'%20stroke='white'%20stroke-width='3.93408'/%3e%3cpath%20d='M15.1792%2015.2236C15.1792%2014.1439%2015.881%2013.0642%2017.1226%2013.0642C18.4182%2013.0642%2018.9041%2014.036%2018.9041%2015.4935V21.1618H22.467V15.0617C22.467%2011.7686%2020.7396%2010.2571%2018.3643%2010.2571C16.5288%2010.2571%2015.6111%2011.2828%2015.1792%2011.9846'%20fill='white'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_215_1247'%3e%3crect%20width='27.6398'%20height='27.6398'%20fill='white'%20transform='translate(0.279785)'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

For Nigeria’s fintech industry, compliance has largely been a buzzword rather than a system that actually controls and monitors activities. As a result, Nigerian fintech companies largely ignored it and prioritised growth. Agent networks scaled rapidly, POS terminals expanded nationwide, and transaction volume dominated investor decks. Compliance existed, but it was woven into the product architecture.

That changed in 2024. The Central Bank of Nigeria imposed heavy monetary penalties, widely reported at ₦1 billion each, on major fintech players over compliance and KYC failures. At the same time, it mandated that POS transactions be routed through licensed Payment Terminal Service Aggregators, embedding regulatory oversight directly into transaction infrastructure.

Alongside the Critical National Information Infrastructure Order and the Nigeria Data Protection Act, a new era began to emerge in the country’s fintech space. An era where compliance will no longer be a back-office function but a core product feature and a competitive moat.

Deep Dive: The New Rules of the Game

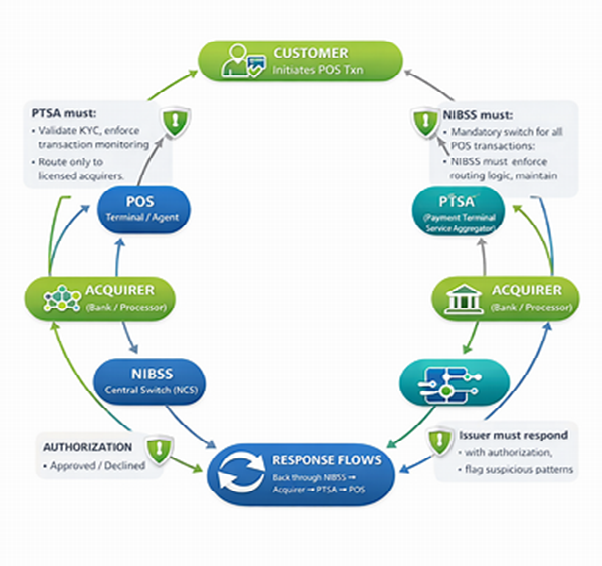

In September 2024, the Central Bank of Nigeria (CBN) directed Payment Service Providers to route POS transactions through CBN-licensed Payment Terminal Service Aggregators (PTSAs), naming NIBSS and Unified Payment Services Limited (UPSL) as the key routing layer. This would be a formal guideline change meant to tighten oversight of electronic transaction processing and standardise POS routing requirements. According to the new directive, routing must pass through the PTSA framework rather than private paths, helping to streamline and track electronic transactions across the country.

What PTSA Integration Actually Means

The practical implication of this directive is that fintechs must now restructure their POS transaction flows to include technical connectivity to licensed PTSAs. This will also include incorporating certification alignment, reporting standardisation, and processor nomination as dictated by the CBN requirements. Rather than directing transactions via privately optimised or internally organised channels, PSPs now have to make sure that transactions traverse validated aggregation layers before settlement. This adds more coordination and streamlined data movement and traceability to the transactions’ lifecycle.

With this, CBN has made routing architecture a regulated infrastructure. The codebase now has compliance built in rather than being addressed at deployment time.

Simultaneously, Nigeria increased its stance on infrastructural and data sovereignty. In June 2024, the federal government signed the Critical National Information Infrastructure (CNII) Order, which designates key systems as critical national assets. Separately, the Nigeria Data Protection Act (NDPA) 2023 codified the concept of privacy governance into law and is enforceable, according to KPMG's briefing. These emerging occurrences have since rendered routing, data management, and governance controlled design limitations and are remaking the way fintech firms conduct their business.

BDC Recapitalisation Signals System-Wide Tightening

In May 2024, the Central Bank of Nigeria significantly revised its regulatory guidelines for Bureau de Change (BDC) operations, introducing a two-tier licensing structure with much higher capital requirements compared with the previous model. Under the updated framework:

- Tier 1 BDC operators must hold a minimum capital base of ₦2 billion, enabling them to operate nationally, open branches, and appoint franchisees.

- Tier 2 BDC operators must maintain a minimum capital base of ₦500 million and operate in only a single state or the Federal Capital Territory.

These thresholds replaced the old single-license minimum of ₦35 million, drastically raising the bar for entry and survival in the BDC space. Most existing operators struggled to meet the new levels ahead of compliance deadlines, demonstrating the CBN’s push for a better-capitalised, more resilient foreign exchange sector.

Key Lessons: Building for Resilience

1. The Data Protection Officer (DPO) is your new best friend

The Nigeria Data Protection Act (NDPA) 2023 formally established the Nigeria Data Protection Commission (NDPC) and introduced enforceable compliance obligations for data controllers and processors. This Act aims to strengthen accountability requirements and regulatory oversight powers. In practice, this shifts the Data Protection Officer (DPO) role from administrative support to strategic governance. The NDPC has also issued operational guidance around compliance structures and the role of Data Protection Compliance Organisations (DPCOs), reinforcing that structured oversight is expected.

For fintechs handling BVN-linked data, transaction logs, or identity verification systems, privacy governance is now directly tied to enforcement risk. To survive or thrive, it is now important to hire a competent DPO and align with a registered DPCO.

2. Early Engagement

Regulatory tightening in 2024 shows that waiting for enforcement is costly. The CBN’s PTSA directive required structured compliance within defined timelines. Proactive engagement with regulators clarifies integration requirements, reporting standards, and licensing expectations before penalties arise. In a climate of stricter oversight, early dialogue reduces ambiguity risk and protects operational continuity.

Conclusion: Compliance as a Trust Signal

The tightening of Nigeria’s regulatory framework in 2024 marks a structural shift in how fintechs will be evaluated. POS routing now sits within licensed PTSA rails. Identity and transaction systems fall under the Critical National Information Infrastructure framework. Data governance is enforceable under the Nigerian Data Protection Act. Far from being temporary oversight cycles, the country hopes to make these durable constraints on how financial technology operates.

Investors must now know that growth metrics alone are no longer sufficient. Infrastructure resilience, routing compliance, governance structures, and documented privacy controls will now influence valuation and risk assessment. A startup that can demonstrate PTSA-aligned architecture, DPO oversight, and regulator engagement signals operational maturity.

As global venture capital cautiously re-enters African markets, capital will likely favour durability over aggression. Compliance is now becoming a signal of trust in Nigeria and across the entire continent.

See Also: Building Investor Trust: Transparency and Governance for African Founders

Loading, please wait...

Share this article on: