Share this article on:

'%3e%3cpath%20d='M0.639648%20-0.000244141H28.2795V27.6396H0.639648V-0.000244141Z'%20fill='black'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M11.0067%205.29028H5.12061L12.0994%2014.5084L5.56705%2022.2413H8.58519L13.5259%2016.3926L17.913%2022.1874H23.7991L16.6175%2012.7014L16.6302%2012.7178L22.8136%205.39793H19.7955L15.2035%2010.8338L11.0067%205.29028ZM8.36963%206.90467H10.2021L20.55%2020.573H18.7176L8.36963%206.90467Z'%20fill='white'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_215_1244'%3e%3crect%20width='27.6398'%20height='27.6398'%20fill='white'%20transform='translate(0.639648)'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

'%3e%3cpath%20d='M0.279785%20-0.000244141H27.9196V27.6396H0.279785'%20fill='black'/%3e%3cpath%20d='M7.94565%209.44696C9.04879%209.44696%209.94306%208.55269%209.94306%207.44956C9.94306%206.34642%209.04879%205.45215%207.94565%205.45215C6.84251%205.45215%205.94824%206.34642%205.94824%207.44956C5.94824%208.55269%206.84251%209.44696%207.94565%209.44696Z'%20fill='white'/%3e%3cpath%20d='M13.4517%2010.4729V21.1617V10.4729ZM7.94531%2010.4729V21.1617V10.4729Z'%20fill='white'/%3e%3cpath%20d='M13.4517%2010.4729V21.1617M7.94531%2010.4729V21.1617'%20stroke='white'%20stroke-width='3.93408'/%3e%3cpath%20d='M15.1792%2015.2236C15.1792%2014.1439%2015.881%2013.0642%2017.1226%2013.0642C18.4182%2013.0642%2018.9041%2014.036%2018.9041%2015.4935V21.1618H22.467V15.0617C22.467%2011.7686%2020.7396%2010.2571%2018.3643%2010.2571C16.5288%2010.2571%2015.6111%2011.2828%2015.1792%2011.9846'%20fill='white'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_215_1247'%3e%3crect%20width='27.6398'%20height='27.6398'%20fill='white'%20transform='translate(0.279785)'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

Unit economics is where ambition meets arithmetic. It is the quiet, often unglamorous layer beneath product launches, pitch decks, funding announcements, and valuation headlines. Strip away the storytelling and branding, and every startup must answer a brutally simple question: Does one customer actually make you money? If the answer is unclear, optimistic, or dependent on perfect macroeconomic conditions, the business is fragile, no matter how impressive the growth chart looks.

In stable economies, founders lean on clean formulas and comforting benchmarks. In volatile markets, however, those same formulas can mislead. Currency depreciation, inflation-driven churn, rising capital costs, and hidden variable expenses distort the true picture of profitability. Understanding unit economics in 2026 requires realism, stress-testing, and a focus on resilience rather than vanity ratios.

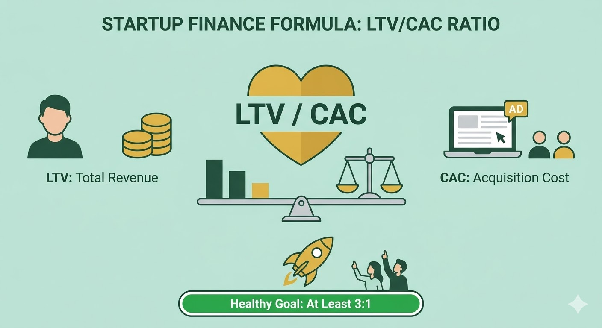

The LTV/CAC “Lie”

At the heart of startup finance lies a familiar equation: Lifetime Value (LTV) divided by Customer Acquisition Cost (CAC). The conventional wisdom is simple - if your LTV/CAC ratio is at least 3:1, your business is healthy.

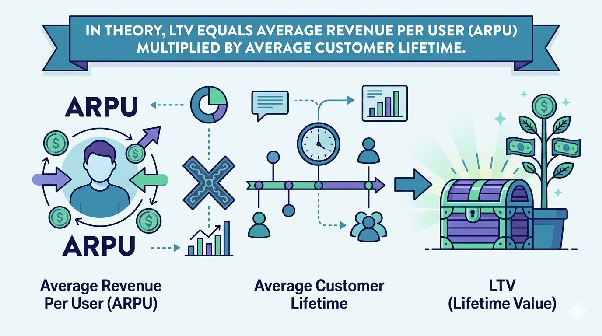

In theory, LTV equals Average Revenue Per User (ARPU) multiplied by average customer lifetime. Acquire a customer for $10, earn $30 over their lifetime, and you are in good shape.

But this rule assumes stability: stable currency, stable inflation, predictable churn, and affordable capital. In volatile markets, these assumptions rarely hold. A startup may show a healthy 3:1 ratio while quietly suffering margin erosion, delayed cash recovery, and increasing churn. This disconnect creates a kind of ghost profitability: profits that show up on dashboards but never translate into durable cash flow.

More important than the ratio itself is the time it takes to recover CAC. A business is highly exposed to macroeconomic shocks when it takes 18 to 24 months to recoup acquisition costs. In high-inflation environments, that delay can destroy value. The safer target is a short payback period; ideally under six months for consumer businesses and under nine months for B2B models. Cash velocity becomes the true measure of health.

Calculating “True LTV” in Volatile Markets

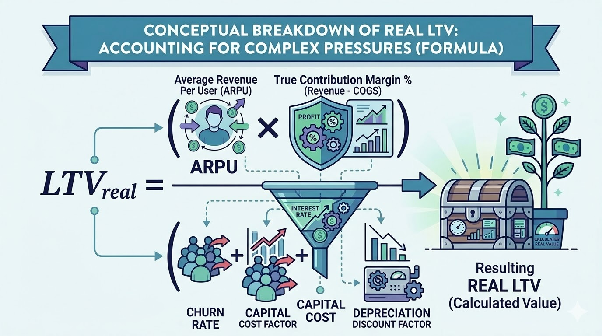

Traditional LTV calculations ignore macroeconomic friction. They assume that today’s revenue retains its value tomorrow and that churn remains constant. In reality, founders must account for three additional forces: currency depreciation, cost of capital, and churn sensitivity.

When the local currency depreciates, it automatically compresses margins if you earn revenue locally but pay key expenses—such as cloud hosting and digital advertising—in USD. A 25 per cent currency decline can significantly reduce real contribution margins without any operational change. Future revenue must therefore be discounted not only by the time value of money but also by expected depreciation.

Cost of capital compounds the issue. Elevated interest rates or investors’ demands for higher premiums reduce the value of future cash flows. Waiting two years to recover CAC in such an environment exposes the startup to funding risk and macro instability.

The practical implication is sobering. Once churn, capital costs, and currency risk are realistically incorporated, LTV often shrinks materially. A business that appeared comfortably profitable may discover its margin of safety is thin. This recalibration is not pessimism; it is disciplined financial modelling.

The 2026 Unit Economics Formula

In volatile environments, a more grounded approach treats churn, cost of capital, and expected currency depreciation as cumulative discount pressures on lifetime value. Conceptually, you can view the Real LTV conceptually as ARPU multiplied by true contribution margin, then divided by the combined pressures of churn, capital cost, and depreciation.

This reframing forces founders to stress-test their assumptions. If churn rises modestly during inflation, lifetime shortens rapidly. If depreciation accelerates, margins narrow. If capital costs remain high, long payback periods erode value.

The goal is not to produce an elegant spreadsheet but to test whether the business model survives realistic downside scenarios. If profitability only exists under best-case assumptions, it is fragile. If it survives under stress, it is resilient.

Segmenting by “Hard” vs “Soft” Revenue

Not all revenue carries equal risk. Some streams are inherently fragile; others are more defensible. Soft revenue typically includes consumer subscriptions, local-currency retail transactions, and discretionary digital services. These are highly sensitive to inflation and income shocks. Churn can spike quickly when consumers reprioritise spending. Hard revenue, by contrast, often comes from B2B contracts, annual enterprise agreements, cross-border clients, or USD-pegged pricing structures. These streams tend to have lower churn and greater predictability. They provide insulation against currency and inflation volatility.

Startups that intentionally “harden” revenue improve their unit economics structurally. Annual prepayments, inflation-adjustment clauses, diversified export revenue, and enterprise pricing strategies all reduce fragility. The objective is not merely revenue growth but revenue durability.

Conclusion: Build for Resilience, Not Ratios

Unit Economics 101 is deceptively simple: acquire customers for less than they generate in profit. But in volatile markets, the calculation demands humility and realism. You must evaluate profitability in real cash terms, adjust it for currency movement, stress-test it against churn spikes, and discount it for capital costs. Startups rarely fail because their LTV/CAC ratio dipped below an arbitrary benchmark. They fail because they run out of cash before recovering CAC, their margins erode under depreciation, or their churn spikes during inflationary cycles. The founders who endure are those who design for volatility rather than hope for stability. They shorten payback periods, harden revenue streams, protect contribution margins, and model downside scenarios honestly.

In 2026 and beyond, true competitive advantage will not lie in aggressive growth alone. It will lie in understanding unit economics deeply enough to build businesses that remain profitable not just in good times, but under pressure.

Loading, please wait...

Share this article on:

Related quiz

Funding and Finance

Quiz: Unit Economics 101 for Startups

How well do you understand unit economics, LTV/CAC, and resilience in volatile markets?