Share this article on:

'%3e%3cpath%20d='M0.639648%20-0.000244141H28.2795V27.6396H0.639648V-0.000244141Z'%20fill='black'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M11.0067%205.29028H5.12061L12.0994%2014.5084L5.56705%2022.2413H8.58519L13.5259%2016.3926L17.913%2022.1874H23.7991L16.6175%2012.7014L16.6302%2012.7178L22.8136%205.39793H19.7955L15.2035%2010.8338L11.0067%205.29028ZM8.36963%206.90467H10.2021L20.55%2020.573H18.7176L8.36963%206.90467Z'%20fill='white'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_215_1244'%3e%3crect%20width='27.6398'%20height='27.6398'%20fill='white'%20transform='translate(0.639648)'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

'%3e%3cpath%20d='M0.279785%20-0.000244141H27.9196V27.6396H0.279785'%20fill='black'/%3e%3cpath%20d='M7.94565%209.44696C9.04879%209.44696%209.94306%208.55269%209.94306%207.44956C9.94306%206.34642%209.04879%205.45215%207.94565%205.45215C6.84251%205.45215%205.94824%206.34642%205.94824%207.44956C5.94824%208.55269%206.84251%209.44696%207.94565%209.44696Z'%20fill='white'/%3e%3cpath%20d='M13.4517%2010.4729V21.1617V10.4729ZM7.94531%2010.4729V21.1617V10.4729Z'%20fill='white'/%3e%3cpath%20d='M13.4517%2010.4729V21.1617M7.94531%2010.4729V21.1617'%20stroke='white'%20stroke-width='3.93408'/%3e%3cpath%20d='M15.1792%2015.2236C15.1792%2014.1439%2015.881%2013.0642%2017.1226%2013.0642C18.4182%2013.0642%2018.9041%2014.036%2018.9041%2015.4935V21.1618H22.467V15.0617C22.467%2011.7686%2020.7396%2010.2571%2018.3643%2010.2571C16.5288%2010.2571%2015.6111%2011.2828%2015.1792%2011.9846'%20fill='white'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_215_1247'%3e%3crect%20width='27.6398'%20height='27.6398'%20fill='white'%20transform='translate(0.279785)'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

The year 2025 marked a definitive structural shift for the African technology landscape, characterised by a fundamental transition of Cleantech from niche impact investing to core infrastructure development towards the continent’s economic future. With over $550M in equity representing a 186% year-on-year surge and $1.1B+ in total capital flowing into the sector, Cleantech became the year’s most consequential investment story, outpacing fintech in growth momentum and redefining what “infrastructure” means for African innovation.

This is the Green Rebound: a fine-tuning of investor priorities, a reordering of sector dominance, and the emergence of energy as the foundational layer for Africa’s next decade of tech growth.

2025: The Year Cleantech Became “Big Tech”

Cleantech’s surge in 2025 wasn’t incremental—it was exponential. Across the continent, the sector attracted close to $1B in funding, driven by a dramatic rise in debt financing and a renewed appetite for asset‑backed business models. Debt financing alone surpassed $1B for the first time, signalling a shift toward structured capital stacks and long‑term infrastructure bets.

According to Forbes Africa, Solar energy alone attracted $830M+, making it the single largest product category in African tech.

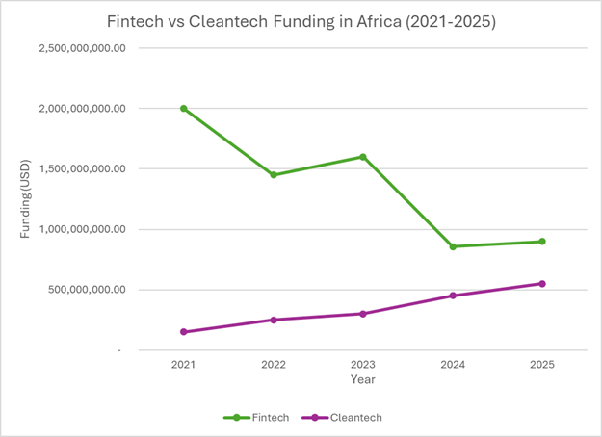

This is the first time cleantech has outpaced fintech in total capital deployed since 2016. The funding gap between the two sectors has narrowed dramatically.

| Year | Fintech (USD) | Cleantech (USD) | Basis |

|---|---|---|---|

| 2021 | $2.0B | $150M | Fintech dominated (62% of all funding); cleantech ~5% share. |

| 2022 | $1.45B | $250M | Fintech confirmed at $1.45B; cleantech rising but still small. |

| 2023 | $1.6B | $300M | Fintech confirmed; cleantech steady growth. |

| 2024 | $857M | $450M | Fintech confirmed drop; cleantech acceleration. |

| 2025 | $900M | $550M | Fintech rebound (est.); cleantech confirmed equity at $550M. |

The Big Four: Why Kenya and Nigeria Lead

While Kenya, Nigeria, South Africa, and Egypt, known as “the big four”, still command 82% of all continental funding, Kenya and Nigeria emerged as the epicentres of the green wave, together attracting hundreds of millions in solar, mobility, and distributed energy deals.

Kenya’s new National Energy Policy 2025–2034 is one of the strongest signals to investors that the country is committed to a long-term clean energy transition. This policy provides a ten-year roadmap with a clear focus on:

- Achieving universal electricity access by 2030

- Expanding renewable energy to 80% of the national grid by 2034

- Establishing domestic green hydrogen capacity by 2032

- Promoting energy storage, smart grids, and clean cooking solutions

- Mobilising local and international green financing

For Cleantech founders and investors, Kenya is now one of the most predictable markets on the continent because the policy’s clarity has reduced the "regulatory risk premium," and boosted investor confidence since 2025.

Nigeria’s persistent national grid instability and massive population have pivotally shifted its focus from pure-play consumer fintech to e-mobility and B2B solar energy.

The Debt Revolution

If equity was the story of 2021, debt was the story of 2025. Cleantech companies, especially those with PAYG models, proved ideal candidates for securitisation, receivables financing, and venture debt. Their asset‑heavy structures and predictable cash flows made them uniquely suited for structured finance.

Case Studies

Sun King’s $156M Securitization

In July 2025, Sun King closed a landmark $156M securitization, the largest commercial‑bank‑backed deal of its kind in Sub‑Saharan Africa. The deal converts future customer repayments into investable assets, enabling the financing of 1.4M solar products, thereby funding more solar home systems and even smartphones.

This allowed the company to scale its fleet to 100,000 units by the end of 2025 without significant equity dilution. Return-seeking, local capital in local currency is essential to unlocking the scale and speed needed to achieve universal energy access. Co‑founder Anish Thakkar emphasised the importance of long‑term capital:

“Distributed solar requires patient capital. These are infrastructure assets with long-term cash flows, not quick flips. When capital aligns with that horizon, scale becomes inevitable.”

Spiro’s E‑Mobility Surge

Spiro secured $100M in asset‑backed financing to scale its electric motorcycle fleet across West Africa. The company expects to surpass 100,000 deployed electric bikes by the end of 2025; a whopping 400% Year-Over-Year jump, thereby marking one of the largest e‑mobility raises on the continent.

d.light’s Receivables Financing

By continuing its multi-year strategy of raising large receivables-backed facilities, such as "Brighter Life," d.light has contributed significantly to the nearly $950M in Cleantech debt recorded in 2025.

These deals illustrate a structural shift: African cleantech is now a debt-driven asset class, not a grant-dependent impact niche.

From Mitigation to Adaptation & Resilience

African founders are rewriting the climate narrative. Across Nigeria, Kenya, and Ghana, national grids are failing more frequently. Therefore, the pitch is no longer about “saving the planet” in that sense; it’s about keeping the lights on. Businesses and households are transitioning to distributed solar, not for sustainability, but for survival.

The collapse of national grids has triggered:

- A massive B2C shift toward home solar systems

- A parallel B2B surge in commercial & industrial (C&I) solar

- A rise in mini‑grids and battery‑as‑a‑service models

Cleantech is no longer climate mitigation; it is economic survival.

The Infrastructure Decade (2026–2035)

Cleantech is becoming the foundational layer for Africa’s next wave of innovation. Three sectors illustrate why:

AI and Green Compute

Africa’s AI future requires massive data centre capacity, which depends solely on energy. Data centres require stable, low‑cost power, which distributed solar and geothermal microgrids can deliver at scale. Without Cleantech, Africa cannot build a competitive computing infrastructure.

E‑Mobility: The Last Mile Flip

By 2026, the transition of "Boda Bodas" (motorcycle taxis) and delivery fleets from petrol to electric will reach a tipping point. With companies like Spiro, which are scaling aggressively in Africa’s e-mobility transformation, battery-swapping infrastructure is now active in cities like Lagos and Nairobi. Hence, the operational cost of an Electric Vehicle is lower than that of its fossil-fuel counterpart.

Climate‑Smart Agriculture

The green rebound is also hitting the soil. Funding is flowing into solar-powered cold storage and drought-resistant supply chain logistics, ensuring that African food systems can survive increasingly erratic weather patterns.

Conclusion: The New Playbook

The 2025 rebound has proven that the "Asset-Light" era of African tech is evolving. While software is still vital, the next generation of African "Unicorns" will likely be asset-heavy, debt-fueled giants. These companies, part utility, part bank, and part logistics providers, are building the physical rails of the continent.

The Green Rebound isn't just a recovery of funding levels; it is the birth of the Foundational Layer. If you want to bet on the future of African AI, Fintech, or Retail, you must first bet on the companies providing the power and the wheels.

Loading, please wait...

Share this article on:

Related quiz

Other

Quiz: The Green Rebound — Africa's 2025 Cleantech Inflection Point

Test your understanding of Africa's 2025 cleantech surge, debt financing trends, and the new infrastructure playbook.