Share this article on:

'%3e%3cpath%20d='M0.639648%20-0.000244141H28.2795V27.6396H0.639648V-0.000244141Z'%20fill='black'/%3e%3cpath%20fill-rule='evenodd'%20clip-rule='evenodd'%20d='M11.0067%205.29028H5.12061L12.0994%2014.5084L5.56705%2022.2413H8.58519L13.5259%2016.3926L17.913%2022.1874H23.7991L16.6175%2012.7014L16.6302%2012.7178L22.8136%205.39793H19.7955L15.2035%2010.8338L11.0067%205.29028ZM8.36963%206.90467H10.2021L20.55%2020.573H18.7176L8.36963%206.90467Z'%20fill='white'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_215_1244'%3e%3crect%20width='27.6398'%20height='27.6398'%20fill='white'%20transform='translate(0.639648)'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

'%3e%3cpath%20d='M0.279785%20-0.000244141H27.9196V27.6396H0.279785'%20fill='black'/%3e%3cpath%20d='M7.94565%209.44696C9.04879%209.44696%209.94306%208.55269%209.94306%207.44956C9.94306%206.34642%209.04879%205.45215%207.94565%205.45215C6.84251%205.45215%205.94824%206.34642%205.94824%207.44956C5.94824%208.55269%206.84251%209.44696%207.94565%209.44696Z'%20fill='white'/%3e%3cpath%20d='M13.4517%2010.4729V21.1617V10.4729ZM7.94531%2010.4729V21.1617V10.4729Z'%20fill='white'/%3e%3cpath%20d='M13.4517%2010.4729V21.1617M7.94531%2010.4729V21.1617'%20stroke='white'%20stroke-width='3.93408'/%3e%3cpath%20d='M15.1792%2015.2236C15.1792%2014.1439%2015.881%2013.0642%2017.1226%2013.0642C18.4182%2013.0642%2018.9041%2014.036%2018.9041%2015.4935V21.1618H22.467V15.0617C22.467%2011.7686%2020.7396%2010.2571%2018.3643%2010.2571C16.5288%2010.2571%2015.6111%2011.2828%2015.1792%2011.9846'%20fill='white'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_215_1247'%3e%3crect%20width='27.6398'%20height='27.6398'%20fill='white'%20transform='translate(0.279785)'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e)

After record funding highs in 2021 and 2022, venture capital inflows into African startups declined sharply by 2024, leading to lower valuations, tighter access to capital, cost-cutting, and a renewed focus on profitability. This correction, however, was not due to a lack of innovation; it was simply a reckoning with mathematics.

According to the African Private Equity and Venture Capital Association’s 2024 Venture Capital in Africa Report, both deal volume and total funding value fell significantly compared to the boom years. Although global monetary tightening was underway, Africa’s case was unique: many fintechs had adopted a Silicon Valley growth model. The problem is that this model was designed for stable currencies, high-margin consumers, and deep capital markets: conditions that do not fully apply in Lagos, Nairobi or anywhere else on the continent.

The Myth of the "One Billion" Consumers

For years, pitch decks opened with Africa’s 1.4 billion population, presenting demographic scale as synonymous with market depth. However, population is not purchasing power. Income across much of sub-Saharan Africa remains a fraction of that in developed markets.

Even in African markets where digital payments have grown rapidly, like Nigeria, financial inclusion gaps, informal-sector dominance, and cash reliance remain structural realities. Digital adoption has accelerated, but the depth of monetizable users is uneven. The assumption that a billion people automatically translates into a billion high-value users inflated Total Addressable Market (TAM) projections during the funding boom. In reality, the “effective TAM,” or the number of users capable of generating sustainable revenue at scale, is often significantly smaller than demographic headlines suggest.

Blitzscaling vs the “Slow Cook”

The Silicon Valley playbook emphasises speed. Acquire users first, worry about margins later. That logic carried over well into Africa’s 2021–2022 funding boom, when fintechs could afford to subsidise transfers, run referral loops, and treat cash burn as a strategic move. But when capital tightened, the model ran into the limits of thin-margin markets. While reporting on this decline, TechCabal mentions that companies will continue to cut costs and focus on unit economics in an uncertain funding environment.

That pattern aligns with the broader global fintech narrative: McKinsey’s “Fintechs: A new paradigm of growth” frames the post-boom period as a move away from pure expansion, toward sustainable value creation. In short, blitzscaling did not fail because African founders were less capable; it failed because speed is only an advantage when the underlying economics can survive once subsidies stop.

The “Dollar Fund, Naira Revenue” Mismatch

Currency exposure was another problem with the imported playbook. Because most African fintechs raised capital in US dollars, they also had to benchmark against dollar-denominated return expectations. The challenge is that their revenues were in local currencies. In Nigeria, exchange-rate volatility between 2023 and 2024 significantly altered the real value of naira earnings when translated into dollars.

Even large, established firms are not immune to FX shocks, as MTN learned in 2025. The impact is much more profound for startups. Cloud infrastructure, software tools, and some talent costs remain dollar-priced, while revenue weakens in dollar terms during devaluation cycles. The Silicon Valley model assumes currency stability, which frontier markets do not guarantee. When a company’s revenue base depreciates while its capital expectations remain dollar-fixed, growth alone cannot resolve the mismatch.

Case Studies of the “Pivot to Reality”

Rather than eliminate the African fintech ambition, this correction further refined it. The contrast between the 2021–2022 consumer neobank wave and the models attracting capital in 2024–2025 clearly illustrates this shift.

During the funding boom, several startups positioned themselves as “neobanks for everyone.” Their value propositions were zero-fee transfers, instant onboarding, debit cards, and lifestyle branding designed to capture young, mobile-first users. The result was rapid growth, aided by marketing spend, discounts, and transaction subsidies.

However, as capital tightened, the underlying economics came under closer scrutiny. Retail neobank models in low-ARPU markets depend heavily on interchange fees, thin transaction margins, and the eventual cross-selling of higher-margin products, such as lending. In environments where transaction values are modest and fraud exposure is persistent, achieving sustainable lifetime value relative to acquisition cost can be challenging.

In contrast, infrastructure-led and B2B-focused fintechs have demonstrated greater resilience. Companies serving merchants, SMEs, and financial institutions operate in higher-average-revenue environments with more predictable transaction flows. In 2024, Moniepoint secured significant investment from global backers, including Google, underscoring investor confidence in models anchored in transaction infrastructure and business enablement. Rather than relying primarily on consumer subsidies, such operators monetise processing, credit, and value-added services embedded into merchant workflows.

The divergence between these models does not imply that consumer fintech lacks long-term opportunity. Instead, it illustrates that the path to sustainability in frontier markets often requires either higher-value customer segments or deeper integration into the financial infrastructure stack. Essentially, it is a pivot toward economic durability rather than away from innovation.

Defining the African Playbook for 2026

The take-home lesson from the 2024–2025 correction is that African fintech cannot simply replicate the assumptions that powered Silicon Valley’s rise. The emerging doctrine for 2026 should be a recalibration of how growth is pursued, rather than an outright rejection of its possibility under prevailing market conditions.

First, positive unit economics have shifted from being deferred milestones to becoming early requirements. Investors who once prioritised scale are now emphasising contribution margins and payback periods. In a 2022 interview with TechCrunch, Iyin Aboyeji of Future Africa argued that founders should “build good businesses rather than chase valuations,” noting that capital discipline and clearly defined unit economics are essential when market conditions tighten. That perspective has become more mainstream as venture funding normalised in 2024 and 2025.

Second, currency awareness is now treated as a strategy rather than an incidental matter. The volatility during recent exchange-rate adjustments reinforced the need for cost structures that can withstand FX shocks. Companies increasingly negotiate localised cost bases, diversify revenue streams, or structure pricing models that reflect currency risk. The expectation of delivering 10x returns on investment in declining revenue environments has prompted more conservative growth modelling and a greater emphasis on margin resilience.

Third, infrastructure depth is gaining priority over surface-level expansion. The funding attracted by infrastructure-led operators, like the previously mentioned 2024 investment in Moniepoint, reflects investor appetite for models embedded within transaction rails and SME ecosystems. Rather than building standalone consumer applications, many fintechs are integrating payments, credit, and financial tools directly into merchant workflows and enterprise systems.

And finally, risk management has moved closer to the centre of product design. Documented fraud patterns underscore the need for robust identity verification, transaction monitoring, and operational controls. In high-adversary environments, sustainable growth depends on embedding risk analytics into the core architecture rather than treating security as an afterthought.

In Conclusion

Together, these elements form a Lagos/Nairobi playbook: disciplined unit economics from inception, currency-aware financial planning, infrastructure-first thinking, and localised risk modelling. It is less dramatic than the blitzscaling narrative that defined 2021, while also more aligned with the structural realities of African frontier markets.

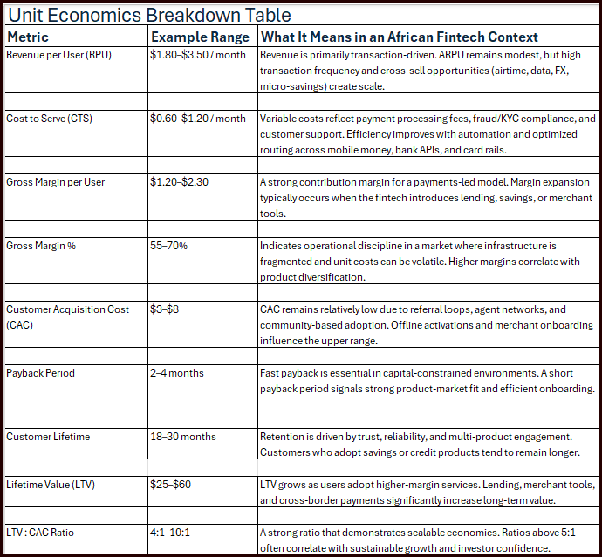

Complete Sample Unit Economics Breakdown Table:

Loading, please wait...

Share this article on: